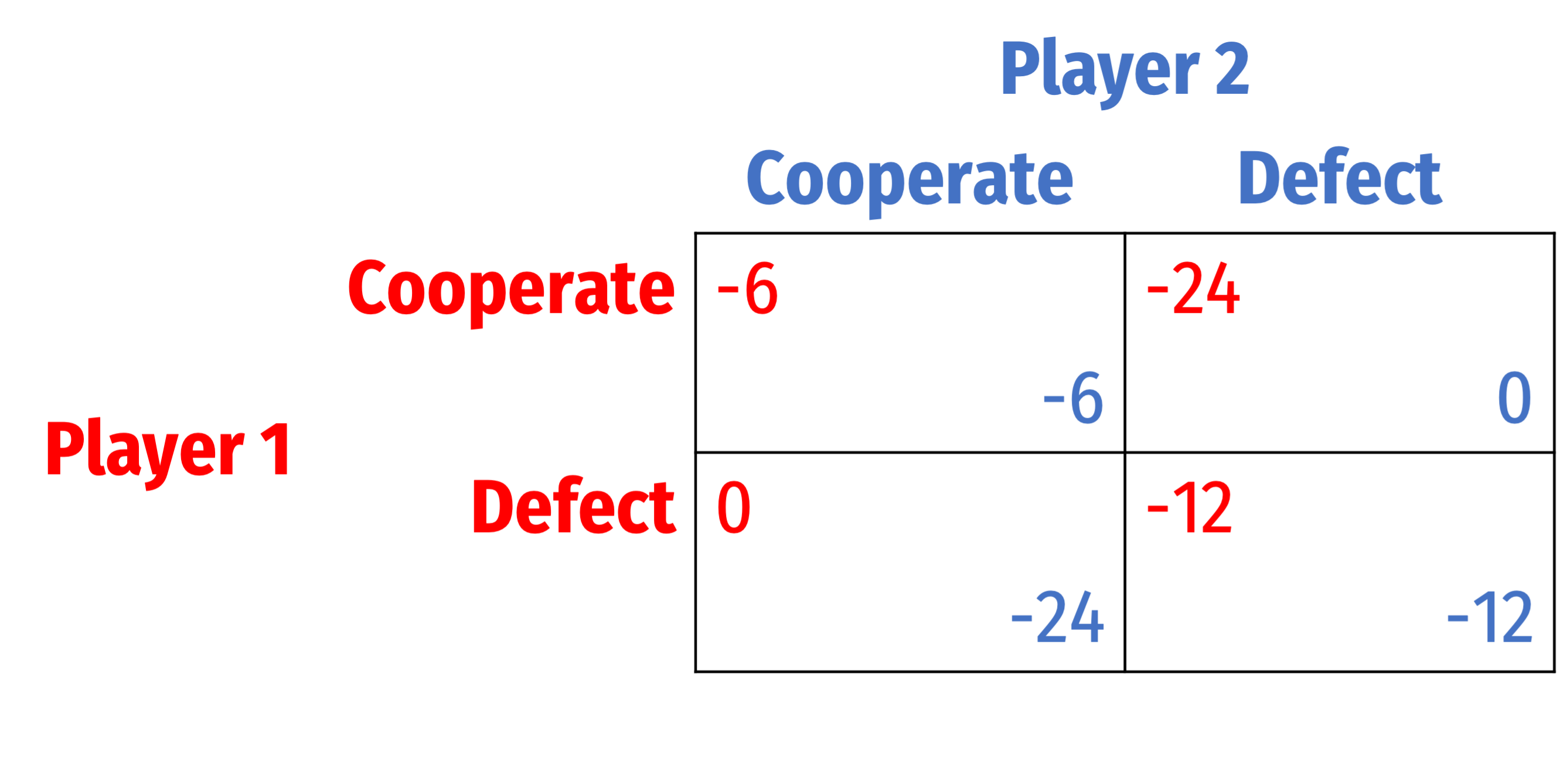

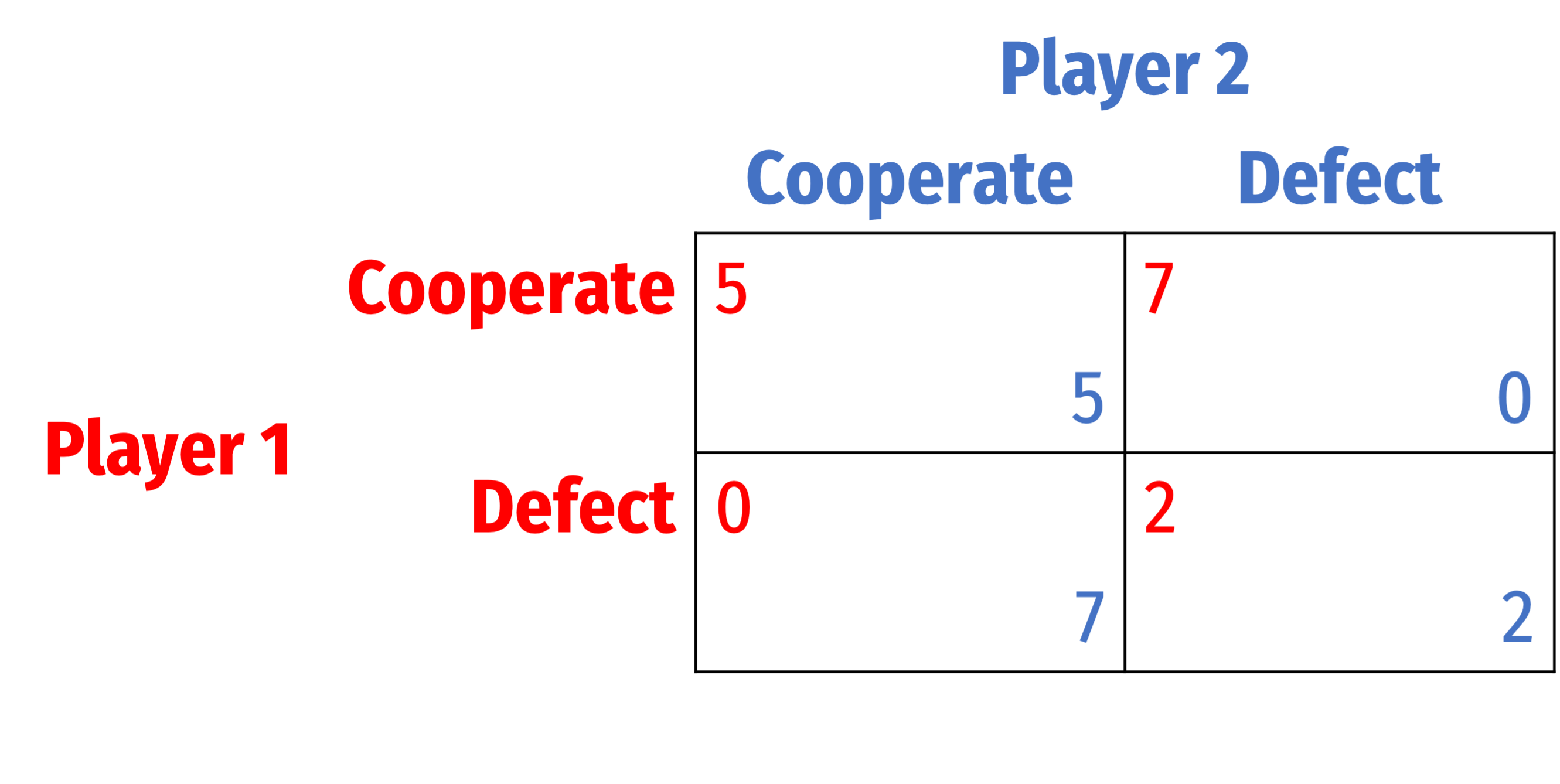

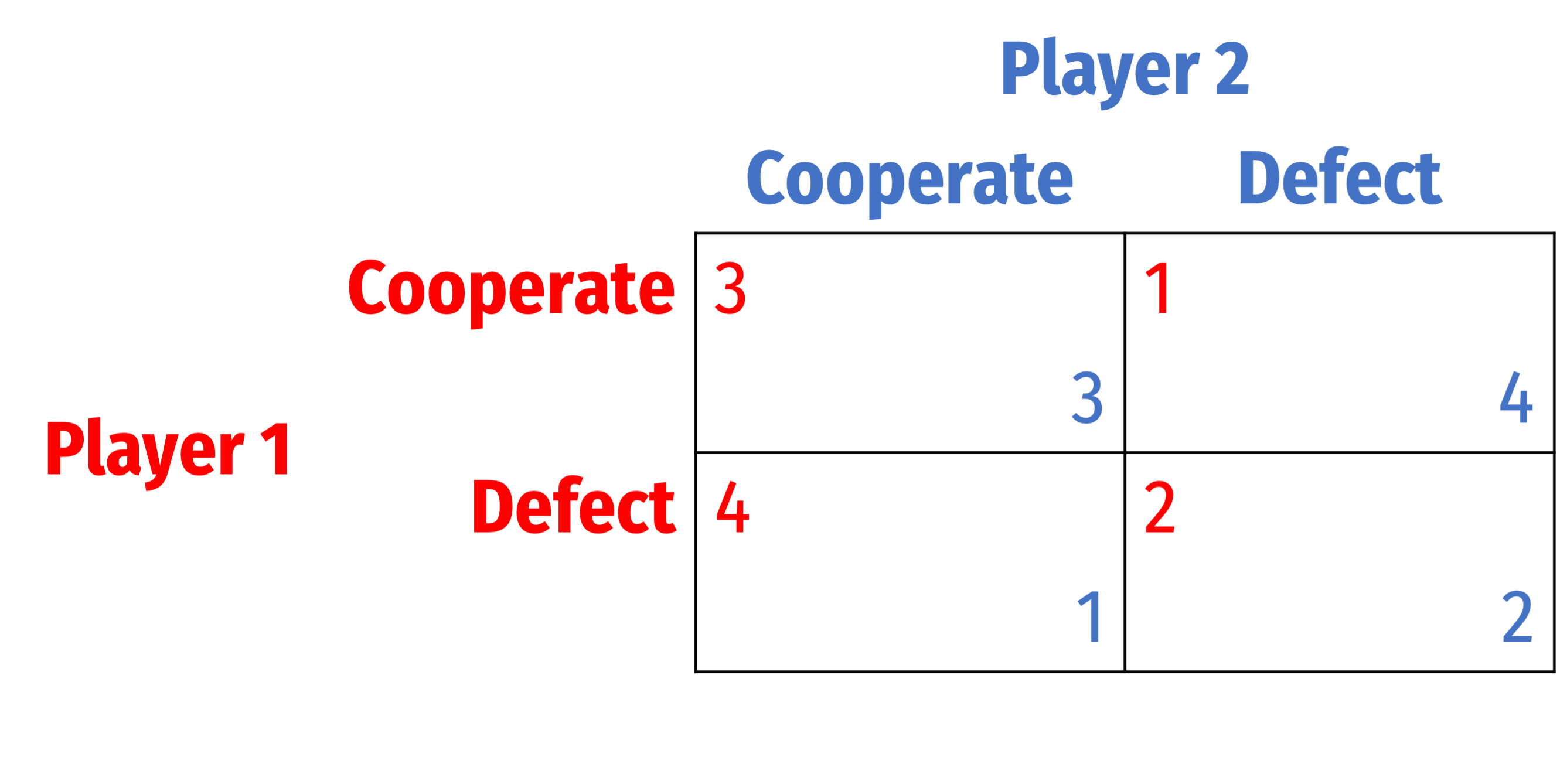

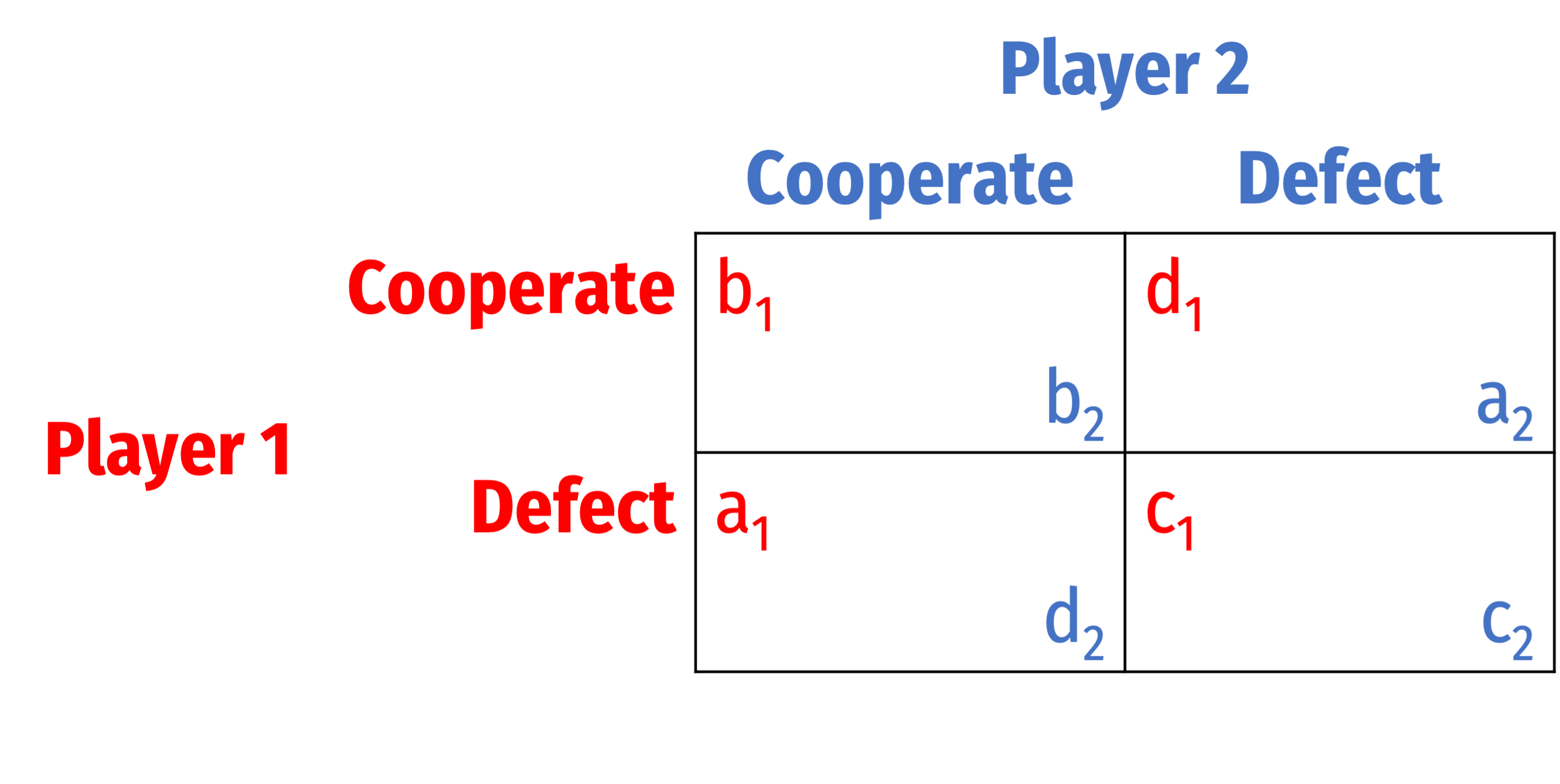

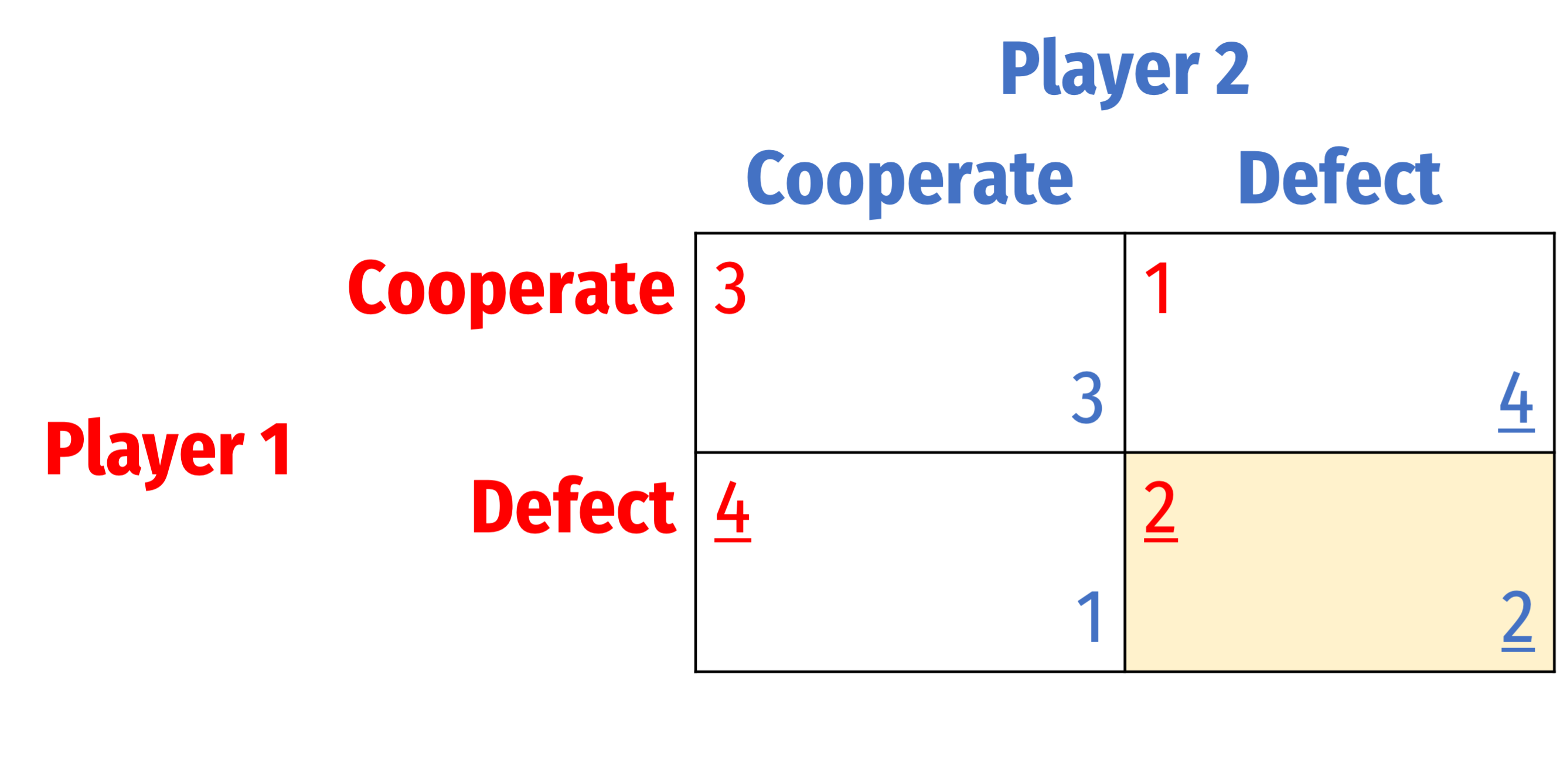

class: center, middle, inverse, title-slide # 1.2 — Essential Micro Concepts ## ECON 316 • Game Theory • Fall 2021 ### Ryan Safner<br> Assistant Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/gameF21"><i class="fa fa-github fa-fw"></i>ryansafner/gameF21</a><br> <a href="https://gameF21.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>gameF21.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Game Theory vs. Decision Theory](#3) ### [Optimization & Preferences](#) ### [Solution Concepts: Nash Equilibrium](#) --- class: inverse, center, middle # Game Theory vs. Decision Theory --- # The Two Major Models of Economics as a “Science” .pull-left[ ## Optimization - Agents have .hi[objectives] they value - Agents face .hi[constraints] - Make .hi[tradeoffs] to maximize objectives within constraints .center[  ] ] -- .pull-right[ ## Equilibrium - Agents .hi[compete] with others over **scarce** resources - Agents .hi[adjust] behaviors based on prices - .hi[Stable outcomes] when adjustments stop .center[  ] ] --- # Game Theory vs. Decision Theory Models I .pull-left[ .center[  ] ] .pull-right[ - Traditional economic models are often called .hi[“Decision theory”]: - .hi-purple[Optimization models] **ignore all other agents** and just focus on how can **you** maximize **your** objective within **your** constraints - Consumers max utility; firms max profit, etc. - **Outcome**: .hi-purple[optimum]: decision where *you* have no better alternatives ] --- # Game Theory vs. Decision Theory Models I .pull-left[ .center[  ] ] .pull-right[ - Traditional economic models are often called .hi[“Decision theory”]: - .hi-purple[Equilibrium models] assume that there are **so many agents** that **no agent’s decision can affect the outcome** - Firms are price-takers or the *only* buyer or seller - **Ignores all other agents’ decisions**! - **Outcome**: .hi-purple[equilibrium]: where *nobody* has any better alternative ] --- # Game Theory vs. Decision Theory Models III .pull-left[ .center[  ] ] .pull-right[ - .hi[Game theory models] directly confront .hi-purple[strategic interactions] between players - How each player would optimally respond to a strategy chosen by other player(s) - Lead to a stable outcome where everyone has considered and chosen mutual best responses - **Outcome**: .hi-purple[Nash equilibrium]: where *nobody* has a better strategy **given the strategies everyone else is playing** ] --- # Equilibrium in Games .pull-left[ .center[  ] ] .pull-right[ - .hi-purple[Nash Equilibrium]: - no player wants to change their strategy **given all other players’ strategies** - each player is playing a **best response** against other players’ strategies ] --- class: inverse, center, middle # Optimization & Preferences --- # Individual Objectives and Preferences .pull-left[ .center[  ] ] .pull-right[ - What is a player's .hi-turquoise[objective] in a game? - “To win”? - Few games are purely zero-sum - “De gustibus non est disputandum” - We need to know a player's .hi[preferences] over game outcomes ] --- # Modeling Individual Choice .pull-left[ - The .hi[consumer's utility maximization problem]: 1. **Choose:** .hi-purple[ < a consumption bundle >] 2. **In order to maximize:** .hi-green[< utility >] 3. **Subject to:** .hi-red[< income and market prices >] ] .pull-right[ .center[  ] ] --- # Modeling Firm's Choice .pull-left[ .smallest[ - 1<sup>st</sup> Stage: .hi-purple[firm's profit maximization problem]: 1. **Choose:** .hi-blue[ < output >] 2. **In order to maximize:** .hi-green[< profits >] - 2<sup>nd</sup> Stage: .hi-purple[firm's cost minimization problem]: 1. **Choose:** .hi-blue[ < inputs >] 2. **In order to _minimize_:** .hi-green[< cost >] 3. **Subject to:** .hi-red[< producing the optimal output >] ] ] .pull-right[ .center[  ] ] --- # Preferences I .pull-left[ - Which game outcomes are **preferred** over others? .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[ .green[**Example**:] Between any two outcomes `\((a,b)\)`: ] ] .pull-right[ .center[  ] ] --- # Preferences II .pull-left[ - We will allow **three possible answers**: ] .pull-right[ .center[  ] ] --- # Preferences II .pull-left[ - We will allow **three possible answers**: .content-box-blue[ 1. .blue[`\\(a \succ b\\)`: (Strictly) prefer `\\(a\\)` over `\\(b\\)`] ] ] .pull-right[ .center[  ] ] --- # Preferences II .pull-left[ - We will allow **three possible answers**: .content-box-blue[ 1. .blue[`\\(a \succ b\\)`: (Strictly) prefer `\\(a\\)` over `\\(b\\)`] 2. .blue[`\\(a \prec b\\)`: (Strictly) prefer `\\(b\\)` over `\\(a\\)`] ] ] .pull-right[ .center[  ] ] --- # Preferences II .pull-left[ - We will allow **three possible answers**: .content-box-blue[ 1. .blue[`\\(a \succ b\\)`: (Strictly) prefer `\\(a\\)` over `\\(b\\)`] 2. .blue[`\\(a \prec b\\)`: (Strictly) prefer `\\(b\\)` over `\\(a\\)`] 3. .blue[`\\(a \sim b\\)`: Indifferent between `\\(a\\)` and `\\(b\\)`] ] ] .pull-right[ .center[  ] ] --- # Preferences II .pull-left[ - We will allow **three possible answers**: .content-box-blue[ 1. .blue[`\\(a \succ b\\)`: (Strictly) prefer `\\(a\\)` over `\\(b\\)`] 2. .blue[`\\(a \prec b\\)`: (Strictly) prefer `\\(b\\)` over `\\(a\\)`] 3. .blue[`\\(a \sim b\\)`: Indifferent between `\\(a\\)` and `\\(b\\)`] ] - .hi[*Preferences*] **are a list of all such comparisons between all bundles** See my ECON 306 [class on preferences](https://micros21.classes.ryansafner.com/content/1.3-content/#appendix-1-material-on-preferences) for more. ] .pull-right[ .center[  ] ] --- # So What About the Numbers? .pull-left[ - Long ago (1890s), utility considered a real, measurable, .hi-purple[cardinal] scale<sup>.hi[†]</sup> - Utility thought to be lurking in people's brains - Could be understood from first principles: calories, water, warmth, etc - Obvious problems ] .pull-right[ .center[  ] ] .footnote[<sup>.hi[†]</sup> "Neuroeconomics" & cognitive scientists are re-attempting a scientific approach to measure utility] --- # Utility Functions? .pull-left[ - More plausibly .hi-turquoise[infer people's preferences from their actions]! - “Actions speak louder than words” - .hi-purple[Principle of Revealed Preference]: if a person chooses `\(x\)` over `\(y\)`, and both are affordable, then they must prefer `\(x \succeq y\)` - Flawless? Of course not. But extremely useful approximation! - People tend not to leave money on the table ] .pull-right[ .center[  ] ] --- # Utility Functions! .pull-left[ - A .hi[utility function] `\(u(\cdot)\)`<sup>.hi[†]</sup> *represents* preference relations `\((\succ , \prec , \sim)\)` - Assign utility numbers to bundles, such that, for any bundles `\(a\)` and `\(b\)`: `$$a \succ b \iff u(a)>u(b)$$` ] .pull-right[ .center[  ] ] .footnote[<sup>.hi[†]</sup> The `\\(\cdot\\)` is a placeholder for whatever goods we are considering (e.g. `\\(x\\)`, `\\(y\\)`, burritos, lattes, dollars, etc)] --- # Utility Functions, Pural I .pull-left[ .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[ .hi-green[Example]: Imagine three alternative bundles of `\((x, y)\)`: `$$\begin{aligned} a&=(1,2)\\ b&=(2,2)\\ c&=(4,3)\\ \end{aligned}$$` ] ] -- .pull-right[ - Let `\(u(\cdot)\)` assign each bundle a utility level: | `\(u(\cdot)\)` | |------------| | `\(u(a)=1\)` | | `\(u(b)=2\)` | | `\(u(c)=3\)` | ] -- - .hi-turquoise[Does this mean that bundle `\\(c\\)` is 3 times the utility of `\\(a\\)`?] --- # Utility Functions, Pural II .pull-left[ .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[ .hi-green[Example]: Imagine three alternative bundles of `\((x, y)\)`: `$$\begin{aligned} a&=(1,2)\\ b&=(2,2)\\ c&=(4,3)\\ \end{aligned}$$` ] ] .pull-left[ - Now consider `\(u(\cdot)\)` and a *2*<sup>*nd*</sup> function `\(v(\cdot)\)`: | `\(u(\cdot)\)` | `\(v(\cdot)\)` | |------------|------------| | `\(u(a)=1\)` | `\(v(a)=3\)` | | `\(u(b)=2\)` | `\(v(b)=5\)` | | `\(u(c)=3\)` | `\(v(c)=7\)` | ] --- # Utility Functions, Pural III .pull-left[ - Utility numbers have an .hi-purple[ordinal] meaning only, **not cardinal** - Both are valid utility functions: - `\(u(c)>u(b)>u(a)\)` ✅ - `\(v(c)>v(b)>v(a)\)` ✅ - because `\(c \succ b \succ a\)` - .hi-purple[Only the .ul[ranking] of utility numbers matters!] ] .pull-right[ .center[  ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - We want to apply utility functions to the outcomes in games, often summarized as .hi[“payoff functions”] - Using the **ordinal** interpretation of utility functions, we can rank player preferences over game outcomes ] .pull-right[ .center[  ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - Take a **prisoners' dilemma** and consider the payoffs to .red[Player 1] - `\(u_1(\color{red}{D}, \color{blue}{C}) \succ u_1(\color{red}{C}, \color{blue}{C})\)` - `\(\color{red}{0} > \color{red}{-6}\)` - `\(u_1(\color{red}{D}, \color{blue}{D}) \succ u_1(\color{red}{C}, \color{blue}{D})\)` - `\(\color{red}{-12} > \color{red}{-24}\)` ] .pull-right[ .center[  ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - Take a **prisoners' dilemma** and consider the payoffs to .blue[Player 2] - `\(u_2(\color{red}{C}, \color{blue}{D}) \succ u_2(\color{red}{C}, \color{blue}{C})\)` - `\(\color{blue}{0} > \color{blue}{-6}\)` - `\(u_2(\color{red}{D}, \color{blue}{D}) \succ u_2(\color{red}{D}, \color{blue}{C})\)` - `\(\color{blue}{-12} > \color{blue}{-24}\)` ] .pull-right[ .center[  ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - We will keep the process simple for now by simply assigning numbers to consequences - In fact, we can assign almost *any* numbers to the payoffs as long as we keep the *order* of the payoffs the same - i.e. so long as `\(u(a) > u(b)\)` for all `\(a \succ b\)` ] .pull-right[ .center[  ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - We will keep the process simple for now by simply assigning numbers to consequences - In fact, we can assign almost *any* numbers to the payoffs as long as we keep the *order* of the payoffs the same - i.e. so long as `\(u(a) > u(b)\)` for all `\(a \succ b\)` ] .pull-right[ .center[  This is the same game ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - We will keep the process simple for now by simply assigning numbers to consequences - In fact, we can assign almost *any* numbers to the payoffs as long as we keep the *order* of the payoffs the same - i.e. so long as `\(u(a) > u(b)\)` for all `\(a \succ b\)` ] .pull-right[ .center[  This is the same game ] ] --- # Utility Functions and Payoffs Over Game Outcomes .pull-left[ - We will keep the process simple for now by simply assigning numbers to consequences - In fact, we can assign almost *any* numbers to the payoffs as long as we keep the *order* of the payoffs the same - i.e. so long as `\(u(a) > u(b)\)` for all `\(a \succ b\)` ] .pull-right[ .center[  This is the same game, so long as `\(a>b>c>d\)` ] ] --- # Rationality, Uncertainty, and Risk .pull-left[ - We commonly assume, for a game: - Players understand the rules of the game - Common knowledge assumption - Players behave .hi[rationally]: try to maximize payoff - represented usually as (ordinal) utility - make no mistakes in choosing their strategies ] .pull-right[ .center[  ] ] --- # Rationality, Uncertainty, and Risk .pull-left[ .smaller[ - Game theory does not permit us to consider true .hi-purple[uncertainty] - Must rule out *complete* surprises (Act of God, etc.) - What do people maximize in the presence of true uncertainty? [Good question](https://micros21.classes.ryansafner.com/content/3.3-content) - But we can talk about .hi[risk]: distribution of outcomes occurring with some known **probability** - In such cases, what do players **maximize** in the presence of risk? ] ] .pull-right[ .center[  ] ] --- # Rationality, Uncertainty, and Risk .pull-left[ - One hypothesis: players choose strategy that maximizes .hi-purple[expected value] of payoffs - probability-weighted average - leads to a lot of paradoxes! `$$E[p] = \sum_{i=1}^n \pi_i p_i$$` - `\(\pi\)` is the probability associated with payoff `\(p_i\)` ] .pull-right[ .center[  ] ] --- # Rationality, Uncertainty, and Risk .pull-left[ .smallest[ - Refinement by Von Neuman & Morgenstern: players instead maximize .hi[expected *utility*] - utility function over probabilistic outcomes - still some paradoxes, but fewer! `$$p_a \succ p_b \iff E[u(p_a)] > E[u(p_b)]$$` - Allows for different .hi-turquoise[risk attitudes]: - risk neutral, risk-averse, risk-loving - makes utility functions .hi-purple[cardinal] (but still not measurable!) - called VNM utility functions ] ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # Solution Concepts: Nash Equilibrium --- # Advancing Game Theory .left-column[ .center[  ] ] .right-column[ - Von Neumann & Morgenstern (vNM)'s *Theory of Games and Economic Behavior* (1944) establishes "Game theory" - Solve for outcomes only of 2-player zero-sum games - Minimax method (we'll see below) ] --- # Advancing Game Theory .left-column[ .center[  .smallest[ John Forbes Nash 1928—2015 Economics Nobel 1994 ] ] ] .right-column[ - Nash's *Non-Cooperative Games* (1950) dissertation invents idea of "(Nash) Equilibrium" - Extends for all `\(n\)`-player non-cooperative games (zero sum, negative sum, positive sum) - Proves an equilibrium exists for all games with finite number of players, strategies, and rounds - Nash's [27 page Dissertation on Non-Cooperative Games](https://rbsc.princeton.edu/sites/default/files/Non-Cooperative_Games_Nash.pdf) ] --- # Advancing Game Theory .left-column[ .center[  .smallest[ John Forbes Nash 1928—2015 Economics Nobel 1994 ] ] ] .right-column[ .center[  ] ] --- # A Beautiful Movie, Lousy Economics .pull-left[ - A .hi[Pure Strategy Nash Equilibrium (PSNE)] of a game is a set of strategies (one for each player) such that no player has a profitable deviation from their strategy given the strategies played by all other players - Each player's strategy must be a best response to all other players' strategies ] .pull-right[ .center[  ] ] --- # A Beautiful Movie, Lousy Economics .center[ <iframe width="980" height="550" src="https://www.youtube.com/embed/CemLiSI5ox8" title="YouTube video player" frameborder="0" allow="accelerometer; autoplay; clipboard-write; encrypted-media; gyroscope; picture-in-picture" allowfullscreen></iframe> ] --- # Solution Concepts: Nash Equilibrium .pull-left[ .center[  ] ] .pull-right[ - Recall, .hi[Nash Equilibrium]: no players want to change their strategy given what everyone else is playing - All players are playing a best response to each other ] --- # Solution Concepts: Nash Equilibrium .pull-left[ .center[  ] ] .pull-right[ .smallest[ - Important about Nash equilibrium: 1. N.E. `\(\neq\)` the “*best*” or *optimal* outcome - Recall the Prisoners' Dilemma! 2. Game may have *multiple* N.E. 3. Game may have *no* N.E. (in “pure” strategies) 4. All players are not necessarily playing the same strategy 5. Each player makes the same choice each time the game is played (possibility of mixed strategies) ] ] --- # Pareto Efficiency .pull-left[ .smallest[ - Suppose we start from some initial allocation (.blue[A]) ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Pareto Efficiency .pull-left[ .smallest[ - Suppose we start from some initial allocation (.blue[A]) - .hi[Pareto Improvement]: at least one party is better off, and no party is worse off - .green[D, E, F, G] are improvements - .red[B, C, H, I] are not ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-2-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Pareto Efficiency .pull-left[ .smallest[ - Suppose we start from some initial allocation (.blue[A]) - .hi[Pareto Improvement]: at least one party is better off, and no party is worse off - .green[D, E, F, G] are improvements - .red[B, C, H, I] are not - .hi[Pareto optimal/efficient]: no possible Pareto improvements - Set of Pareto efficient points often called the .hi-green[Pareto frontier]<sup>.magenta[†]</sup> - Many possible efficient points! ] .tiny[<sup>.magenta[†]</sup>I’m simplifying...for full details, see [class 1.8 appendix](https://microf20.classes.ryansafner.com/files/CT_Application_2_Exchange.pdf) about applying consumer theory!] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Pareto Efficiency and Games .pull-left[ - Take the **prisoners’ dilemma** - .hi-purple[Nash Equilibrium]: (.hi-red[Defect], .hi-blue[Defect]) - neither player has an incentive to change strategy, *given the other's strategy* - Why can’t they both **cooperate**? - A clear .hi-purple[Pareto improvement]! ] .pull-right[ .center[  ] ] --- # Pareto Efficiency and Games .pull-left[ - Main feature of prisoners’ dilemma: the Nash equilibrium is Pareto inferior to another outcome (.hi-red[Cooperate], .hi-blue[Cooperate])! - But that outcome is *not* a Nash equilibrium! - Dominant strategies to **Defect** - How can we ever get rational cooperation? ] .pull-right[ .center[  ] ] --- # Nash Equilibrium and Solution Concepts .pull-left[ - This is **far** from the last word on solution concepts, or even Nash equilibrium! - But sufficient for now, until we return to simultaneous games - Next week, **sequential games**! ] .pull-right[ .center[  ] ]